Charter at $125: A 32% Implied IRR, or a Company the Market Expects to Disappear?

Shares of Charter Communications [CHTR] have fallen hard over the past several months. In my previous post (the Polaroid piece, here), I made an argument that applies to every company, all of the time: a share price is never just a number—at any given moment, it carries an implied Internal Rate of Return (IRR), the return a long-term owner signs up for if he buys at that price and then collects the business’s cash flows over its entire life. Charter is a vivid, live example of the very same idea. When its shares traded near $125, the implied IRR on RIM’s base-case scenario climbed above 32% per year. To put that in human terms: achieving such a level of return is the equivalent of doubling your money every 2.7 years. (I walk through how a given IRR translates into real, compounded returns over time here.)

A number like that should make any rational investor stop and ask the obvious question: what would have to be true for it to be deserved?

What Counts as a Base-Case Fair Value

The whole exercise hinges on this, because an implied IRR is only as meaningful as the cash-flow forecast standing behind it. So before anything else, what does a reasonable base case for Charter look like?

Start by being honest about what Charter is. Like every cable operator, it is no longer in the television business in any meaningful sense—it is a data provider that happens to own a coaxial network. The relevant arena, then, is broadband, and broadband is genuinely contested. I recently laid out how the alternatives stack up on the two variables a customer actually cares about—internet speed and cost—across fiber, cable, 5G (and 4G LTE) fixed wireless, and Starlink-style low-earth-orbit satellite. The conclusion is not the one the share price implies. Fiber is faster, but it is expensive to build and remains far from universal. Fixed wireless from the mobile carriers (T-Mobile, Verizon, AT&T) is cheap and simple to install, but it is capacity-constrained—a real threat in specific pockets rather than a wholesale replacement. Satellite is a genuine answer for the rural edge that wire and tower never reach, at a price and latency that keep it a niche. Against all three, cable still delivers fast, low-latency, near-ubiquitous service at a competitive price. This is a maturing business facing real competition—not a melting ice cube.

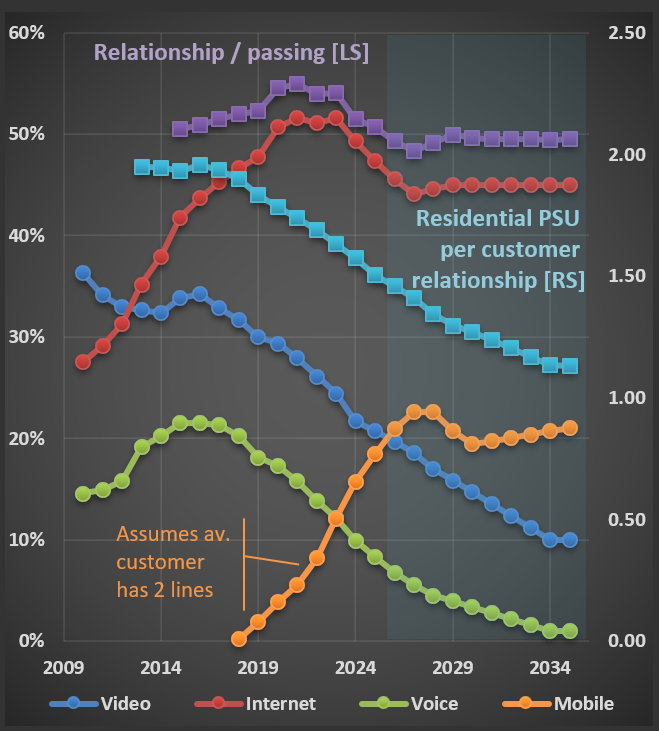

You can see the maturity directly in the chart below. Internet penetration—the line that matters—has plateaued near 50% after years of climbing. Video and voice keep doing what they have done for a decade (fading), and mobile is the one product still gaining. In my Charter work I already carry a roughly 500-basis-point loss of internet penetration to competition inside the base case. In other words, the saturation the Market is anxious about is not a surprise to the forecast; it is built into it.

The Market Is Pricing Charter to Disappear

It is entirely reasonable to assume that internet penetration eventually stabilizes—every adoption curve does. What is not reasonable is the conclusion the current price draws from that. The Market, at these levels, is effectively assuming Charter will cease to exist.

Here is the arithmetic that exposes it. In RIM’s base case, once Charter’s capital spending falls back to a normal maintenance level—the heavy build-out phase of any network is finite, by definition—the free-cash-flow yield on the shares is over 40%. Read that one more time: a single year of free cash flow would buy back almost half the entire company, if the shares simply stayed where they are today. A 40%-plus FCF yield is not the price of a slow-growing, mature business; it is the price of a business the Market expects to vanish. And even when I press the model harder—stripping out another 500 basis points of internet penetration on top of the loss already embedded in the base case—the implied IRR still lands squarely in the range of a typical undervalued position at RIM.

The Market Exists to Serve You, Not to Teach You

This is a very unusual price distortion, and it is worth naming the instinct it triggers. When a stock falls this far, the comfortable assumption is that “the Market knows best”—that the price is telling you something you have missed. I would gently push back on that, because it is simply not a reasonable approach to investing. The same Market was happy to pay more than $800 for a share of Charter at the end of 2021—for a business that, operationally, looks much the same today as it did then. A mechanism that prices the identical company above $800 and then below $125 in the span of a few years is not a teacher. It is a counterparty in a mood.

That is the entire point: the Market does not exist to teach you; it exists to serve you. It will swing wildly from greed to despair and back, and each swing is an offer—to buy, or to sell, on favorable terms. The challenge, as always, and as is the case with any genuine investment rather than speculation, is not to interpret the Market’s mood. It is to do the harder, quieter work of correctly forecasting the financial future of the company in front of you. Get that right, and the price is simply the opportunity the Market happens to be handing you while you wait.