A Polaroid Redux? What the $5.7 Trillion Chip Rally Forgets to Ask

A colleague recently sent me a Wall Street Journal article asking how much further the chip rally can run, now that US chipmakers are collectively worth around $5.7 trillion (here). It is a well-written piece, and worth reading. But, as is almost always the case with this kind of coverage, it frames the whole debate around the wrong question.

The article does what most market commentary does: it debates forward price-to-earnings multiples, contrasts bull and bear price targets, and tries to decide whether the rally has been “earnings-driven” or “multiple-driven.” These are useful shortcuts. But they are only shortcuts. Not once does the article ask the one question that should matter to anyone actually buying these businesses: at today’s price, what Internal Rate of Return (IRR) is an owner signing up for, if he holds the company and collects its cash flows over its entire life?

That omission is not a small one. A multiple is a simplification—a single number standing in for an entire stream of future cash flows, growth assumptions, margins, and capital needs. It can be a handy reference, but it tells you almost nothing about the return embedded in a price. I made this exact point a few months ago when the WSJ ran a similar piece on Walmart (here): the author leaned entirely on forward P/E, when what an investor should care about is the IRR the price implies. The names change—Walmart, chipmakers—but the analytical gap is identical.

A Small Example With an Enormous Lesson

To show what I mean, let me use a company that operated on a far smaller scale than today’s AI giants but illustrates the very same concept: Polaroid.

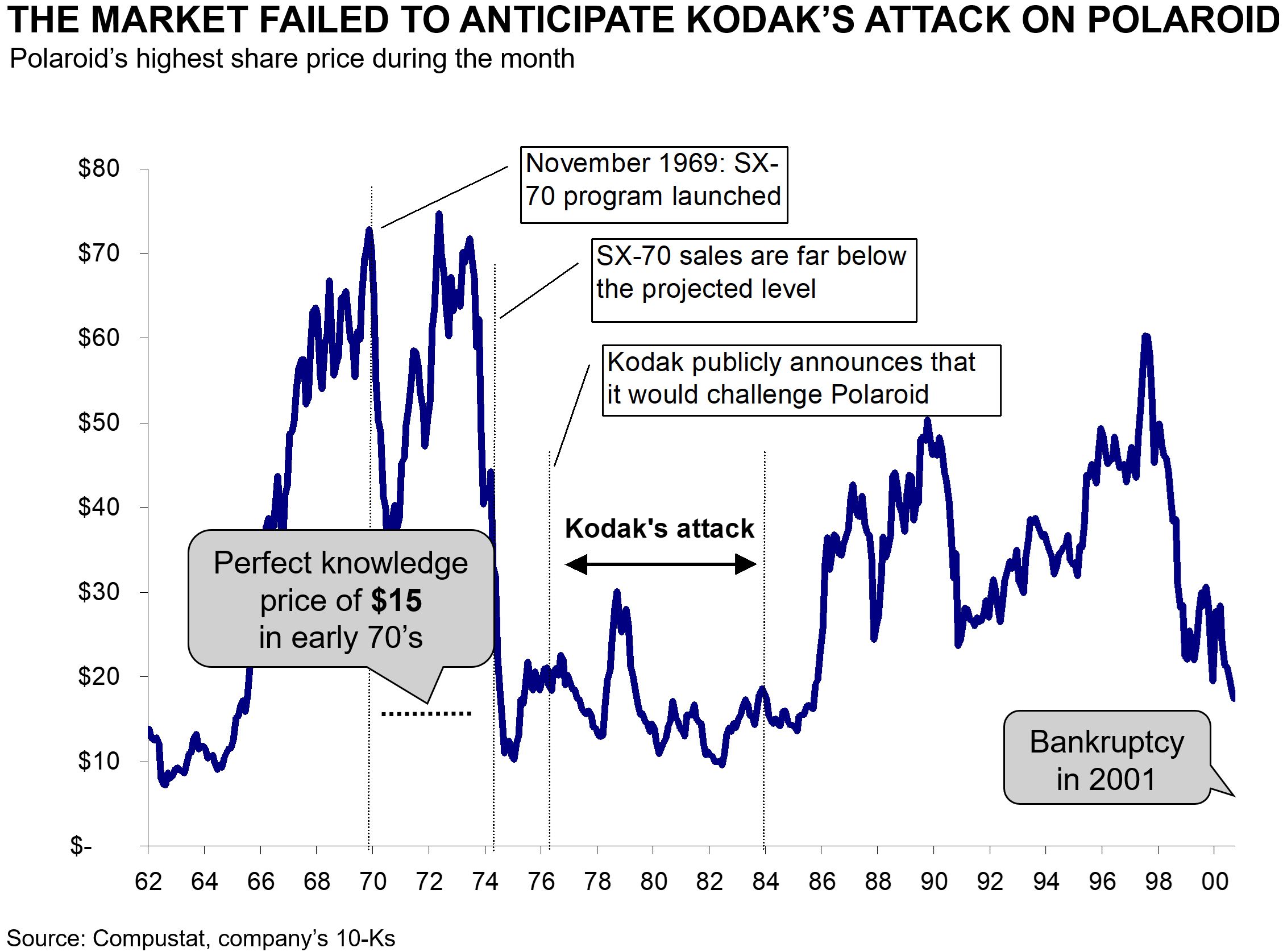

In the early 1970s, the media and analysts were amazed by Polaroid’s new “high-tech” camera, the SX-70. Magazine after magazine described it as a “pocketful of miracles”—a constellation of technical triumphs in optics, dye chemistry, and micro-electronics. Sound familiar? Replace “camera” with “accelerator” or “GPU,” and you could be reading this morning’s coverage of the chip sector.

The enthusiasm pushed Polaroid’s shares to roughly $70 in those years. Here is the uncomfortable part—and the reason this example is so instructive. We now have something we never have in real time: Polaroid’s entire life is over (the company went bankrupt in 2001). That means we know every single dollar of cash flow it ever delivered to its owners. With that complete record in hand, I can calculate what I call the “perfect-knowledge price”—the price you would have had to pay back in 1970 to earn a normal long-term IRR (the 10%–11% I keep coming back to) by owning the business outright. That price was about $15 per share. At $70, the stock was the very definition of a bubble.

These two Polaroid charts, by the way, are not new to me. They come from a case competition I worked on at McKinsey in 2001—a full 25 years ago. I keep them around as a reminder of something I find worth saying out loud: I have been applying this very same concept—comparing a share price to its perfect-knowledge value—across my entire finance career.

Notice what the second chart also shows: the Market completely failed to anticipate Kodak’s attack on Polaroid’s franchise. This is the rule, not the exception. Narratives about a dominant, world-changing technology almost never price in the competitor, the substitute, or the cycle that eventually arrives. (I wrote about a near-identical pattern—Beyond Meat—in my post on speculation versus investment, here.)

What a Share Price Should Actually Reflect

Here is the principle, and it applies to 100% of companies—public or private, AI-related or not. The perfect-knowledge price of any business is the price that, given everything the company will ever pay its owners, produces an IRR in line with what is observed across comparable companies in the same “system” (say, the US). For the names in RIM’s Circle of Competence, that observed IRR clusters tightly: the average across the companies I follow is 10.7%, with a standard deviation under 2%. And, as you would expect, it correlates with each company’s cost of equity (Ke). It is a distribution, not a single magic number—but it is a narrow one.

That last point is what makes the exercise so powerful, and so deflating for bubble enthusiasts. If company after company, across decades and across industries, ends up delivering owners something close to 10%–11%, it is simply illogical to assume that a basket of stocks priced today to deliver far less than that is “normal” or “fairly valued.” The perfect-knowledge price is calculable: it is the cash flow to the shareholder discounted at something near 10%–11%. (Those figures are nominal, so they embed inflation; in a higher-inflation regime, the number may run a touch higher in the coming years. I walk through how a given IRR translates into real, compounded returns over time here.)

Back to the Chips

So the right way to read the $5.7 trillion headline is not “how much further can the multiple expand?” It is: at today’s prices, what IRR is an owner of these businesses actually accepting? I have little doubt that several AI-related names are in a bubble today—Polaroid-style, just with more zeros (the memory makers being an obvious candidate). They could even keep climbing another 5,000x; manias are not bound by arithmetic in the short run. But the long run is different. One day we will know each of these companies' full cash-flow history, just as we now know Polaroid’s. On that day, someone will be able to draw the same chart I drew above—the share price against the perfect-knowledge price—and the gap will speak for itself. “We will know”—someone, someday, will. I already plan to be retired by then.

I would rather not wait that long to find out whether I overpaid. That is why I spend my days estimating, company by company, what the price implies for the owner—rather than arguing over whether 28x or 35x forward earnings is “cheap.” As I have shown before with the 1990s tech bubble (here), the investors who waved away rich valuations because the “technology” was real still earned poor returns. The technology being real was never the question. The price always was.