$VMC [Vulcan Materials]: A $20/Ton Promise—and a Few Reasons for Skepticism

Last week, Vulcan Materials hosted its 2026 Investor Day. The headline number? Management told investors they see a path to $20 per ton of aggregates cash gross profit—roughly double where they are today. Standing on the floor of the NYSE, the CEO put it this way: “just two and a half years ago, our average selling price was less than $20.” Now they expect to make that much in profit per ton.

That deserves a closer look.

The Long, Slow March from $7 to $11

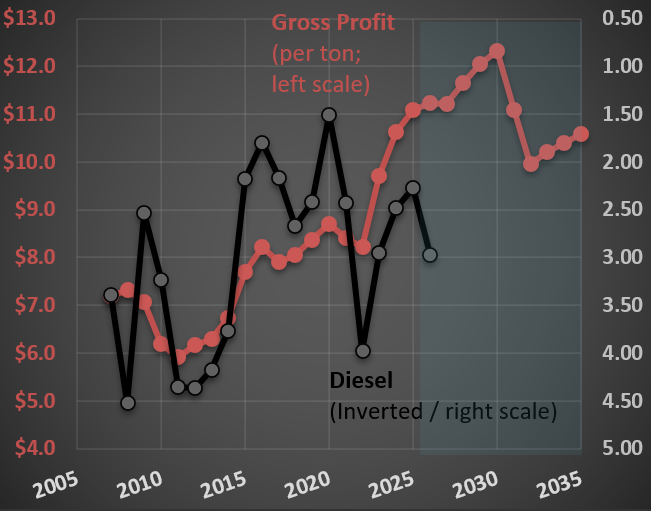

Before getting excited about the next double, it’s worth remembering the journey to where they are. The picture below summarizes it nicely.

It took Vulcan roughly seven years to go from $7 of cash gross profit per ton (in the pre-housing-crisis days) to $8. That period included the housing collapse, a multi-year recovery, and a meaningful tailwind from low diesel prices. Diesel matters here—it’s directly about 10% of operating costs and indirectly much more (trucking, asphalt, plant power). The black/gray line on the chart is diesel inverted: when diesel is cheap, aggregates margins benefit, and you can see the two lines move together for long stretches.

Then came the pandemic. Inflation everywhere—fuel, parts, labor. Aggregates producers responded by raising prices aggressively, and Vulcan rode that wave from $8 to $11 in just a few years. To management’s credit, they handled the inflation passthrough well. But it’s worth being honest about what drove the jump: it wasn’t structural genius—it was a once-in-a-generation inflationary environment that gave the entire industry cover to push prices simultaneously.

Now Comes the $20 Target

So what’s the path to $20? Management says high-single to low-double-digit annual growth in cash gross profit per ton, against demand growing at “low single digits.” They’ve promised more real price improvement than historical averages and lower real cost increases than historical averages. Both at the same time. The implied adjusted EBITDA roughly doubles to $4.5–5.0 billion (from $2.3 billion in 2025).

Two things make me skeptical:

First, every aggregates producer—and a few new entrants—is busy expanding capacity. Read any of Vulcan’s competitors' transcripts and you’ll find the same enthusiasm and the same playbook. When everybody and their mother is pouring capital into the same business, the historical pricing discipline that supports those margins gets harder to defend, not easier. Vulcan itself has acquired 36 aggregate operations and completed 7 greenfields in the past 3.5 years. They’re not the only ones.

Second, the demand story leans heavily on two narratives that have become load-bearing in nearly every industrial company presentation: AI and data centers. These terms came up at the Investor Day 28 times! The CEO described energy projects “to feed data centers and support the age of artificial intelligence” as a coming tailwind to aggregates intensity.

I’ve written before about why I think this is mostly a story, not a number. In this post, I showed that data center construction—even at its current historical peak—accounts for slightly above 2% of total US construction spending. The money in data centers is in the chips and servers inside the buildings, not in the aggregates underneath them. That doesn’t make data centers irrelevant to the broader economy; it means they’re nowhere near large enough, on the construction side, to move the needle for a company like Vulcan Materials.

The Familiar Pattern

This isn’t unique to Vulcan. I noted something similar with $FLS recently (here), where mentioning “nuclear” 25 times in an earnings deck added 30% to the share price for a company with roughly 3.5% nuclear exposure. The mechanic is the same: associate the business with a hot narrative and let multiples do the work.

To be fair, Vulcan is a quality company with irreplaceable assets, real pricing power in concentrated markets (while the FTC is sleeping at the wheel), and a management team that has executed well over a long stretch. Going from $11 to $20 requires some combination of (i) sustained broad-based inflation that the whole industry gets to ride, (ii) genuinely structural improvements in unit economics that haven’t quite shown up in 70 years of company history, and (iii) a demand environment meaningfully better than what management itself describes as “low single digits.”

The history of capital-intensive cyclical businesses hitting targets that depend on simultaneously beating both real price and real cost expectations is not encouraging.