America's Declining Motorcycle Market and What It Means for Harley Davidson

Bloomberg is conducting a comprehensive series of special segments on $HOG [Harley Davidson], highlighting significant shifts in the American motorcycle market - hence this post. The evolution of motorcycle sales per capita in the United States has shown a staggering decline over recent years, as illustrated in the chart below.

Surprisingly, Americans now purchase fewer large motorcycles (over 600cc) than Europeans, despite having advantages that traditionally supported motorcycle ownership: abundant open spaces for riding, widespread garage availability for storage, and higher income per capita. This represents a fundamental shift in the American motorcycle culture that Harley Davidson has long dominated.

As part of my ongoing analysis of recreational vehicle markets, I’m currently researching $BC [Brunswick Corporation], a leader in the marine industry. I’ll be sharing insights on the boating sector soon, examining whether similar consumption pattern changes are occurring across different recreational vehicle categories.

Carter's 2025 Forecast vs. Reality: A Humbling Lesson in Long-Term Guidance

Companies usually provide “guidance” for short term expectations. It helps when there are more complex changes in the P&L (for instance, after an acquisition and/or disposal). But sometimes, they provide longer-term guidance, as did $CRI (Carter’s) management in early 2021. The picture below shows their guidance for 2025 (on the left). On the right, what might happen (as we are now entering the “target year”). The delta between expectations vs. reality is significant (and I’m using a “normalized margin” for 2025 - the actual is expected to be closer to 7%). This example underscores how difficult it is to make forecasts. If it is that hard for a company’s management team that sells baby clothes, founded 160 years ago, can you imagine your chances to forecast sales and profitability in the technology field correctly? If you want to invest (instead of speculate), focus on mundane businesses. And even so you will be humbled by your mistakes!

US Census Bureau Revisions Shrink America's Youngest Population: Implications for Carter's Future Market

When I’m working on $CRI [Carter’s], I need to update the forecasted population growth for the “zero to 5” segment in the US (done by the US Census Bureau), as they are the company’s core “clients.” The first chart below shows—per various group ages—how many millions of people the US has had and is expected to have over the next few decades.

The yellow arrow highlights the “zero to 5” group. Just below it is the “6 to 10” group. Note that the US Census Bureau drops the number of young children in the US with each dataset revision. The second chart gives you an idea of how much: in 2022, the “zero to 5” group’s estimate was reduced by almost 9%!

Glass Half Full: OI's Strategic Pivot Promises Value Amid Historic Low P/E

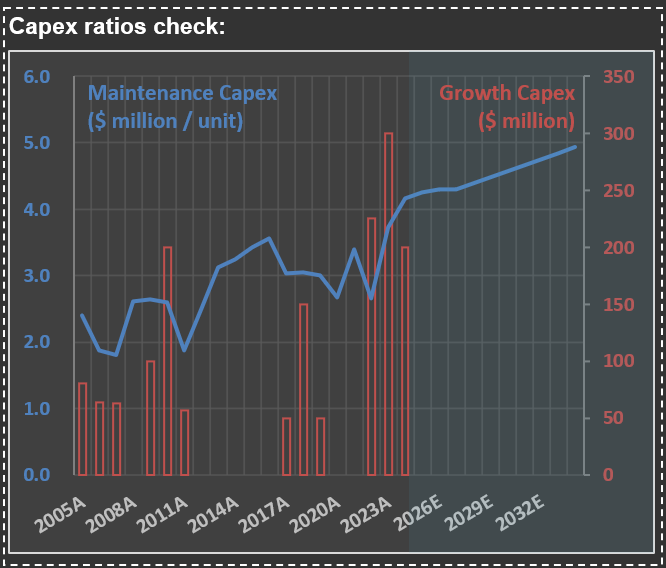

Never underestimate how much money CEOs can burn (and still be paid millions to do so!). Below is my check for Capex for $OI [OI-Glass], the biggest glass containers manufacturer in the world. The company battled massive asbestos liabilities for years. When that got solved, what was the prior CEO plan? Burn almost $1 billion (these are the sum of the two last groups of the red bars) in a new technology called MAGMA.

Here is what the new CEO just said about it: “With regard to MAGMA, we continue to ramp up production at our first greenfield line in Bowling Green, Kentucky. The achievement of key operating and financial milestones at this site over the course of 2025 will be critical as we chart the future of the MAGMA program. As we focus on these milestones at Bowling Green, we have paused the development of Generation 3. As with any capital project, MAGMA will be required to generate returns of at least WACC plus 2%. We will provide more details on our long-term strategic plan next month at our Investor Day.”

In other words, MAGMA didn’t work (as I’m assuming it doesn’t generate returns above WACC). So I will be in New York on March 14th - at the NYSE - to participate on the company’s Investor Day. I hope they will provide information that will increase investors confidence. As of now, if they achieve their $1.45 billion EBITDA guidance for 2027, it means that the company is trading at less than 3x P/E! I don’t use multiples to calculate fair values for companies at RIM. But such a low figure called my attention!

Stanley Black & Decker: Sales Slump and Margin Collapse in the Post-Stimulus Reality

The first picture below shows sales for $SWK (Stanley Black & Decker) - see how it is now below the mid-trendline (which includes the impact from inflation + population growth). The second picture shows margins - it is amazing how strongly impacted their margins were when it became clear that management misinterpreted the excessive stimulus of 2020/2021.

Stanley Black & Decker's Balance Sheet Battle: Unwinding Pandemic-Era Inventory Excesses

I’m working on $SWK [Stanley Black & Decker] today. It is incredible to see what the pandemic did to key lines of companies' balance sheets. The chart shows a massive drop in “inventory turns” (red line) in 2021, meaning that the company overproduced (and ordered excessively from manufacturing partners) tools and whatever it sold. They are bringing inventory to more normal levels, but it will be a multi-year exercise. Accounts Payable (blue line) are close to normal levels but look at the massive peak during the pandemic.

J.B. Hunt's Equipment Dilemma: Pandemic Expansion Meets Post-Boom Reality

Look at what $JBHT management said during the last conference call: “…we still have really significant capacity that’s underutilized. And the cost to store that equipment is a significant headwind for us. And so as we continue to scale and grow our volumes, while also improving pricing, that’s going to be our focus and our effort. The Walmart equipment, we reported – I think we reported just over 122,000 containers at the end of 4Q. When we onboarded the Walmart equipment, all of that equipment requires a modification and we haven’t completed that work. Clearly, we just did the acquisition in, I think, the second quarter of – or end of first quarter, second quarter last year. And that equipment is tucked away in storage right now because frankly, we’re still trying to grow into the 122,000 containers that you can see we own today.”

This was a classic over-investment situation, given the strong cycle for trucking companies during the pandemic (mostly on pricing, as companies were willing to pay anything to secure transportation capacity). The result: a very low “Net PP&E turnover”—see the blue line on the chart. It is as low as in the deep recession years of 2009.

J.B. Hunt: Share Price Defies Earnings Gravity - Market Optimism or Pandemic Memory Bias?

For most companies, share prices follow short-term EPS (in other words, the Market doesn’t anticipate much—it just reflects what it sees “as of now”). It isn’t different for $JBHT — see how the share price follows expected EPS on the chart. However, the current market price appears to be fighting a substantial decline in earnings. Maybe it’s because trucking companies made a disproportional amount of money during the pandemic, biasing some investors regarding how much they are willing to pay for J.B. Hunt’s earnings.

Fleet Age Dynamics: How J.B. Hunt's Minor Aging Shifts Drive Major Truck Purchase Swings

I’m working on $JBHT [J.B. Hunt] today. It is incredible how relatively small fluctuations in the average age of a trucking company’s fleet (represented by the dashed blue line on the chart) change the demand for new trucks. The company went from buying almost 6,000 trucks in 2021/2022 to something close to 3,600 trucks now.

Trucking Tonnage Trends: What ATA Data Reveals About Economic Momentum

Trucking tonnage data from the American Trucking Association (ATA) reveals a persistent sluggishness in demand for trucking services. Take a look at the long-term perspective in the chart below, which helps contextualize current industry conditions within historical patterns.

The visualization offers valuable insights into freight movement trends—often considered a bellwether for broader economic activity. For those monitoring economic signals, this data point merits attention alongside other indicators when evaluating the current business cycle position.